If you’re one of the people who lived through the 2008 financial meltdown, hearing that “another recession may be on the horizon” probably doesn’t make you feel warm and fuzzy. It’s hard to overstate the destruction that the Great Recession had in its crushing 18-month span. Approximately 8.7 million people lost their jobs, and 7.3 million families lost their homes to foreclosure, according to data from RealtyTrac.

Today, we are at the other end of the spectrum. It’s been a long expansionary period in terms of economic growth. But what goes up must eventually come down, or so that’s the thinking of 70% of economists surveyed by the National Association for Business Economics, who predict a recession will occur before the end of 2021. The stock market has been flat and wildly fluctuating since early 2018. Uncertainty about Trump’s trade war with China, the Federal Reserve lowering interest rates, and global power shakeups like Brexit don’t help the creeping feeling of instability.

Naturally, people are wondering if the housing market will crash the same way it did in the 2008 recession—or worse?! While every recession is different and hard to predict, the good news is that many experts agree that housing won’t play as big a role in the next recession. In fact, analysis from ATTOM Data Solutions showed that recessions don’t always spell doom for the housing market. Home prices only decreased in two out of the last five recessions—the one in 1990, and 2008—and increased during the other three recessionary periods.

Related Article: When Is the Best Time of Year to Sell Your House?

So, it’s not always a given that the housing market will be adversely affected during a downturn, and certain economic conditions that caused the last crash don’t exist today. Here’s a look at how the housing market has changed since 2008.

The Lending Landscape is Different

The 2008 housing meltdown was caused by the subprime mortgage crisis. Lending standards were lax at the time, and there were a large variety of loan products to choose from. Because of a surplus in housing, banks were driven to give mortgage loans out to unqualified buyers.

The most infamous loan product of all was the adjustable-rate mortgage (ARM), which would keep payments low for the first two years. Then, the monthly payments and interest rate would skyrocket. That left homeowners saddled with an expensive mortgage payment and pushed them into foreclosure when they couldn’t pay it.

Washington’s own local bank, Washington Mutual, was well-known for these types of ARM loans. It branded itself as your friendly neighborhood bank, but WaMU was much more than a local bank at the time—it was the nation’s fifth largest bank with a presence in 15 states. According to The Balance, only 14 percent of WaMu’s business came from home loans, but those mortgages were so risky they tanked the whole company. WaMu famously filed for bankruptcy in September 2008 and was sold to JP Morgan Chase for a fraction of its worth.

Related Article: How Does Zoning Affect Property Value in Seattle?

Today’s standards are very different. The risky loan products have been replaced by basically two options—fixed rate, or an ARM that meets Qualified Mortgage (QM) standards set forth by the Consumer Financial Protection Bureau. The interest rates are capped so they can’t go up too quickly. You’ll need to make at least a 3.5% down payment, and if your credit score is below 760, you’ll pay a higher interest rate. If your credit score is below 620, you probably won’t qualify for a mortgage at all. You will also have to submit documentation for everything, read required disclosures and observe mandatory waiting periods to make sure you have time to ask questions about your loan terms.

In Seattle, the housing market has cooled considerably this year, but in recent years it was a mad dash against multiple buyers for nearly every property. And the one thing all these buyers had in common? They were all highly qualified. If they were not outright cash buyers, they were making a 20%+ down payment. They were fully underwritten by their lender, meaning every nook and cranny was verified. Last August, the Seattle Times reported that one fourth of Seattle homeowners owned their home outright with no mortgage debt. The mortgage lending landscape today simply doesn’t compare to 2008.

There is a Housing Shortage, Not a Boom…

Some people worry we’re in another housing bubble. Statistically, we’re not. In 2005-06, housing construction was at a peak. The US had approximately 2.2 million housing starts (a measure of future construction of new residential homes or apartment buildings). Homebuilders were building homes at a pace that outpaced supply. Housing starts are an important indicator of economic activity, because if people are buying houses, they’re also probably buying related goods and services.

Related Article: Pros and Cons to Fixing a House Up VS Selling As Is

US Housing Starts Chart

Source: tradingeconomics.com

Realtor magazine recently reported that homebuilding activity is half of 2005 levels. That’s a matter of costs and labor shortages, says Erik Franks, senior vice president at John Burns Consulting. “Cost increases at every step of the way have pushed home prices to a point where home builders find it very difficult to build homes priced $250,000 and below in places where most people want to live.” That’s certainly true in Seattle, where the September median home price hovered around $675,000.

One year ago, Seattle King County Realtors Association spoke with Windermere Chief Economist Matthew Gardner, who said, “We’re not in a housing bubble. Buyers today are overqualified. They’re putting down larger down payments, and they’re not defaulting on their mortgages.” Still, the fundamentals of the market are strong and economists expect moderate home price growth through 2020.

Home Equity Is Stronger Than Ever

Since there has been a longer stretch of growth in the latest economic boom (versus the buying frenzy in the early aughts), homeowners have had more time to acquire equity in their homes. CNBC reported in August that Americans are sitting on a record amount of “tappable” equity—$6.3 trillion. Tappable equity is money homeowners could pull out of their home and still have 20% equity leftover.

Another distinction is that homeowners are largely sitting on that equity rather than cash-out refinancing or getting a home equity line of credit. Tax laws changed in 2018 making it harder to write off interest on a home equity line of credit unless you used the proceeds specifically for home improvement. According to the article, 89% of refinances in 2006 were cash-out. Today, that number is only 61%. Andy Walden, director of market research at mortgage data company Black Knight, says that, “Perhaps the need to tap that equity is a little bit lower and there is a little bit more discipline among consumers.”

Related Article: What is an “Instant Offer” on Your House and How Does it Work?

Foreclosures are Decreasing

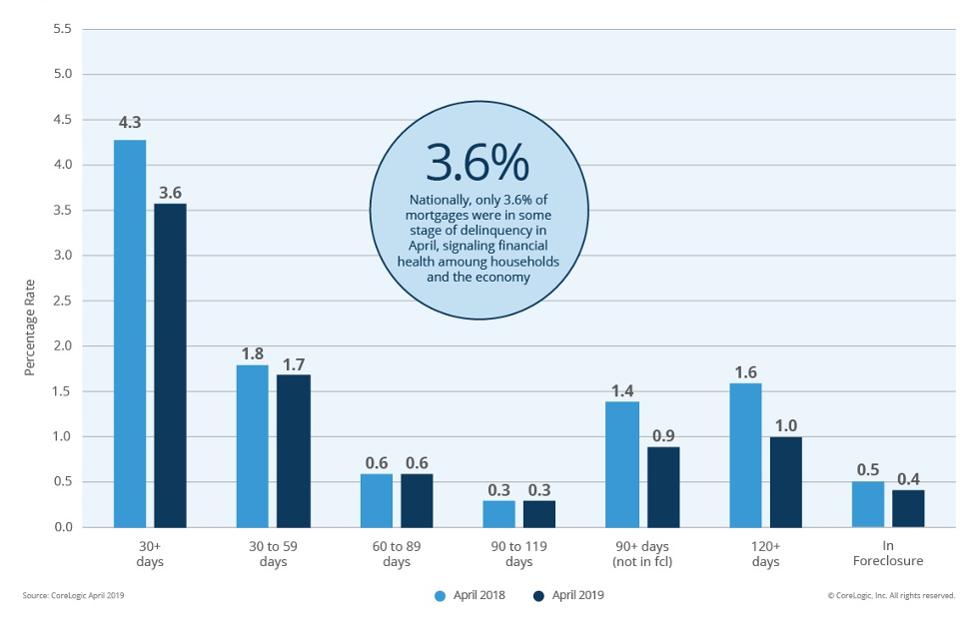

Source: CoreLogic

Foreclosures are another marker that can tell you if the housing market is on shaky ground. Foreclosures are currently at historic lows. Data from CoreLogic showed that in April 2019, only 3.6% of mortgages were in a stage of delinquency. That was down from April 2018 at 4.3% and was the lowest month recorded in 20 years.

The nation’s strong job market and economic growth comes into play here. The most recently reported unemployment rate was 3.5% in September. That marks a 50-year low for unemployment. More people have jobs or can get better-paying jobs, which means less homeowners will be defaulting on their mortgages.

What the Experts Say

More and more lately, real estate industry economists have been speaking out about the possibility of the next recession and what role housing will play in it this time. In July, Zillow surveyed 100 real estate industry experts who agreed that a recession may be coming in the next two years. However, only 12% thought that it would be due to the housing market.

Related Article: 3 Things to Know When Renovating Your Home

Here’s a sampling of what some other real estate economists have said:

“This is going to be a much shorter recession than the last one. I don’t think the next recession will be a repeat of 2008. The housing market is in a better position.”

“This time we won’t have bad mortgages, just people who are losing jobs. We don’t have the scale of the subprime mortgage volume that we did last time around. And we also don’t have massive oversupply – that is a big issue”

—Lawrence Yun, Chief Economist at National Association of Realtors

“Housing slowdowns have been a major component, if not catalyst, for economic recessions in the past, but that won’t be the case the next time around, primarily because housing will have worked out its kinks ahead of time. Housing markets across the country are already heading into a potential correction a solid year before the overall economy is expected to experience the same,” Olsen said. “The current housing slowdown is in some ways a return to balance that will help increase the resiliency of the housing market when the next recession does arrive.”

What to Look Out For

While it’s never fun to live through a recession and face the prospect of losing a job or another detrimental life event, there are actions you can take now to prepare yourself to weather the storm. Focus on paying down debts and saving money. Look at your job stability. It may be a good time to boost your skills or update your resume.

Whether you’re a homeowner or an aspiring homebuyer, keep your eyes on market trends to see where the housing market is expected to go. Keep tabs on Seattle by reading the latest Seattle Housing Market Update. Don’t bet on home prices cratering in the next recession. The prevailing wisdom is that the next recession will be shorter, different and not involve housing or mortgages quite as much.

Need to Sell Your Seattle Area House? Get a COMPLIMENTARY Property Analysis:

Trackbacks/Pingbacks